Internal Sales: Employee Ownership Trusts (EOTs) vs Traditional Management Buyouts (MBOs)

Introduction

When shareholders contemplate an exit from their company, there are two routes that are often considered; sell to an external party or consider selling the business internally to the team working in the business.

External sales involve marketing the company to potential acquirers, which could encompass a range of entities such as companies, private equity firms, or venture capitalists.

On the other hand, internal sales involve selling the business to its own employees, which can include the core management team or the entire workforce.

We have seen an increasing popularity of looking internally when considering the future of the business to secure its legacy and independence. There are two options when considering selling your business to your employees: Management Buyouts (MBOs) and Employee Ownership Trusts (EOTs). This article considers the pros and cons of each of these options:

Management Buyouts (MBOs)

A traditional Management Buyout (MBO) occurs when the existing management team, often with the support of external lenders, acquires the business from its current shareholders. This results in the management team (e.g. two or three key management personnel) becoming the new owners and taking full control of the company's operations and strategy.

Benefits of an MBO

· Industry Knowledge: The existing management team already possesses an understanding of the business, industry, and operations, which can lead to a smoother transition.

· Speed of Transaction: An MBO will typically allow for a quicker exit as the acquirers have already been identified (external sales require an acquirer to be established).

· Flexibility: An MBO provides the current shareholders with the flexibility to selectively determine which employees will be included in the MBO arrangement.

· Reward Staff: An MBO empowers the current shareholder(s) to offer their staff the chance to become owners of the business.

Challenges of an MBO

· Funding Challenges: Securing the necessary funds for an MBO requires financial support from lenders to cover a portion of the transaction. This will increase the level of debt in the company.

· Less Consideration: Typically, MBOs tend to command a lower price compared to what could potentially be attained though a sale to the open market.

· Tax Benefits: MBO sales yield fewer tax advantages for current shareholders compared to sales to an Employee-owned Trust (EOTs). However, it's worth noting that current owners might still be eligible for certain tax reliefs, such as the Business Asset Disposal Relief (BADR). This relief permits the initial £1 million capital gain to be subject to a favourable 10% tax rate (unless this allowance has already been utilised by the shareholders).

Employee Ownership Trusts (EOTs)

Employees Ownership Trusts (EOTs) are a government initiative introduced by the Finance Act 2014 to encourage employee ownership in companies.

An all-employee trust will own a controlling stake in the company which is set up for the benefit of the employees. The employees will not directly own the company.

An EOT is run by its trustees, with their main responsibilities to oversee the profit-sharing policy, loan note repayments and reviewing the company’s financial performance. They represent the interest of the employees by maximising their engagement and commitment to the company. The trustees commonly comprise of a mix of employees, independent professionals and perhaps the original vendor (at least until they are repaid).

The management team will continue to lead the company day-to-day. The trustees do have control over the trading company’s directors and their remuneration.

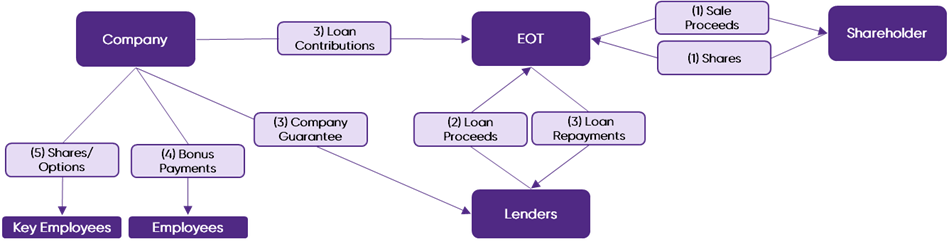

Process of Setting up an EOT

1. The current shareholders (vendors) sell between a 51% to 100% shareholding to the EOT.

2. The EOT pays for the shares using proceeds from third-party financing and vendor loan notes.

3. Vendors receive an upfront payment funded by the initial borrowing and loan note repayments from the company over an agreed period. The company generally secures any loan with its assets.

4. Employees are eligible to receive income tax-free annual bonus payments provided conditions are met.

5. Optional – the Company may consider issuing shares or options to key management or employees.

Benefits of an EOTs

· Tax Advantages: the sale of shares to a EOT will not be liable to capital gains tax (CGT) provided specific conditions are met.

· Employee Engagement and Motivation: EOTs can increase employee engagement, motivation, and a sense of ownership in the success of the company. Employees have a direct stake in the company's performance and can benefit financially from its growth.

· Reward Staff: An EOTs empowers the current shareholder(s) to offer all staff the chance to become stakeholders in the business.

· Speed of Transaction: Like an MBO, EOTs will typically allow for a quicker exit as the acquirers will be the employee trust.

Challenges of an EOTs

· Funding Challenges: Securing the necessary funds for an EOT requires financial support from lenders to cover a portion of the transaction.

· Less Consideration: like MBOs, EOT sales tend to command a lower price compared to what could potentially be attained though a sale to an open market.

· Less Flexibility: the current shareholders cannot offer the sale to certain team members; all will have a shareholding on a equitable basis.

Choosing the right approach.

When current shareholders opt for an internal sale, they face yet another decision—choosing what type of internal sale. This choice is contingent upon a multitude of factors, encompassing the size of the business, its industry, the employee base, and the owner's individual preferences. Business owners are urged to meticulously assess their objectives, the dedication of their workforce, and the legacy they wish to leave behind.

The difference between the two approaches discussed primarily are on flexibility and tax implications. EOTs may impose certain limitations on who assumes ownership following the transaction, yet they often present a more tax-efficient avenue for the current shareholders.

How BSN can help

Facilitating MBOs/EOTs Sales: Providing support to both shareholders and the company throughout the transaction process, which encompasses clarifying the procedure and the advantages to all stakeholders.

Guidance on MBOs/EOTs: Guiding the company on how the company/EOT should be governed following the transaction.

Provide an independent share valuation: Using a combination valuation technique, BSN can estimate a fair market valuation of the company which will need to be approved by HMRC under both techniques.

Legal Assistance: Review all legal documentation and support the legal team in ensuring the proposed transaction is correctly represented in any paperwork.

Tax Assistance: Obtain tax clearance to ensure compliance and provide support when considering tax efficiencies

Assist in providing key employees with share options: Support in implementing other share schemes the company sees beneficial (for example EMI scheme)

External Sales: BSN can also explore options which involve an external sale if preferred or an internal sale does not seem viable.

Please also feel free to request an EOTs information pack which includes more detailed information (such as the specific tax benefits).